The Rules Just Changed For Crypto

Where crypto capital flows meet market intelligence.

📅 Tuesday, March 24, 2026 | Est. read time: 7-8 minutes

TL;DR

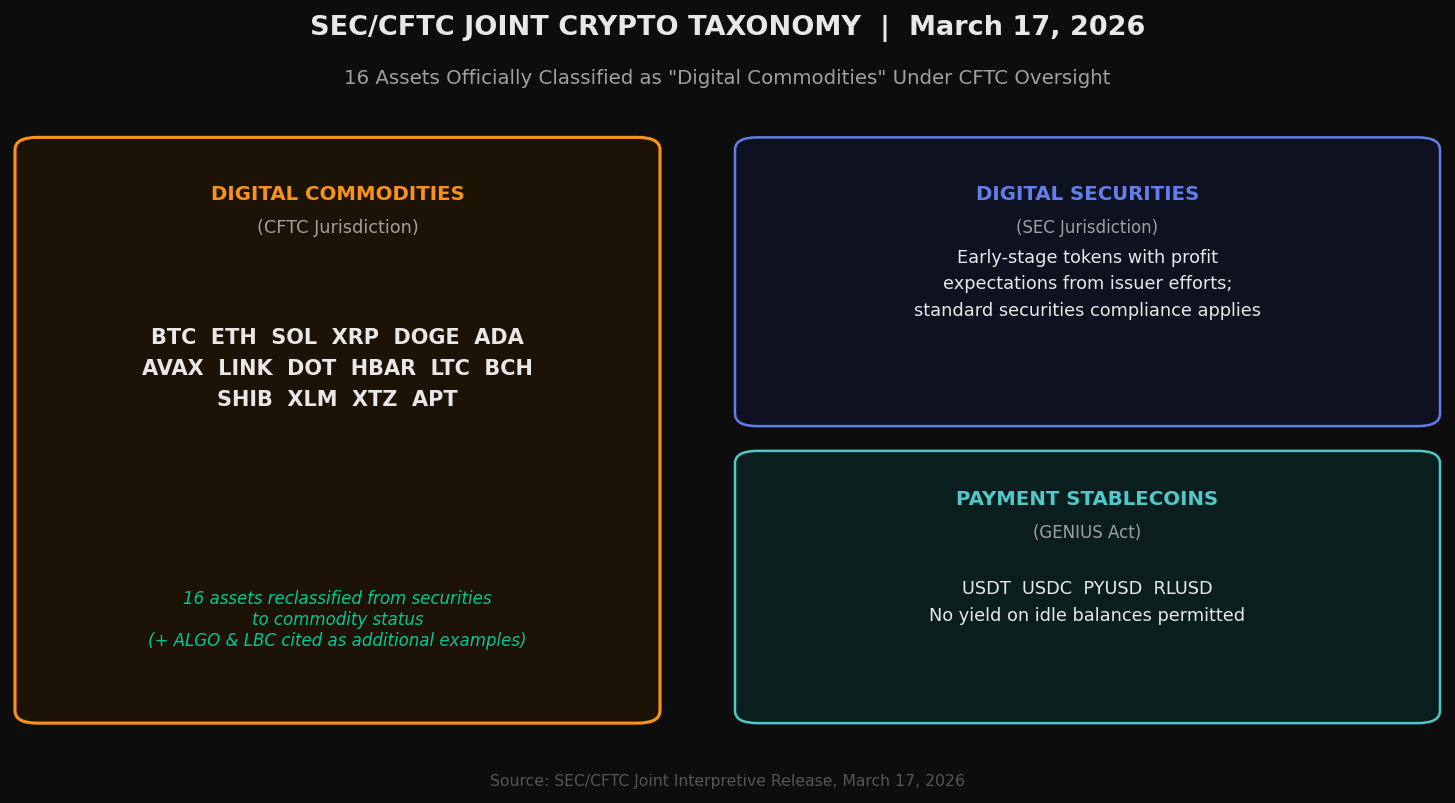

The SEC, in coordination with the CFTC, released a landmark 68-page regulatory taxonomy on March 17, explicitly naming 16 cryptocurrencies as “digital commodities” under CFTC oversight, with Algorand and LBRY Credits cited as additional examples, citing the most significant U.S. regulatory development in crypto history.

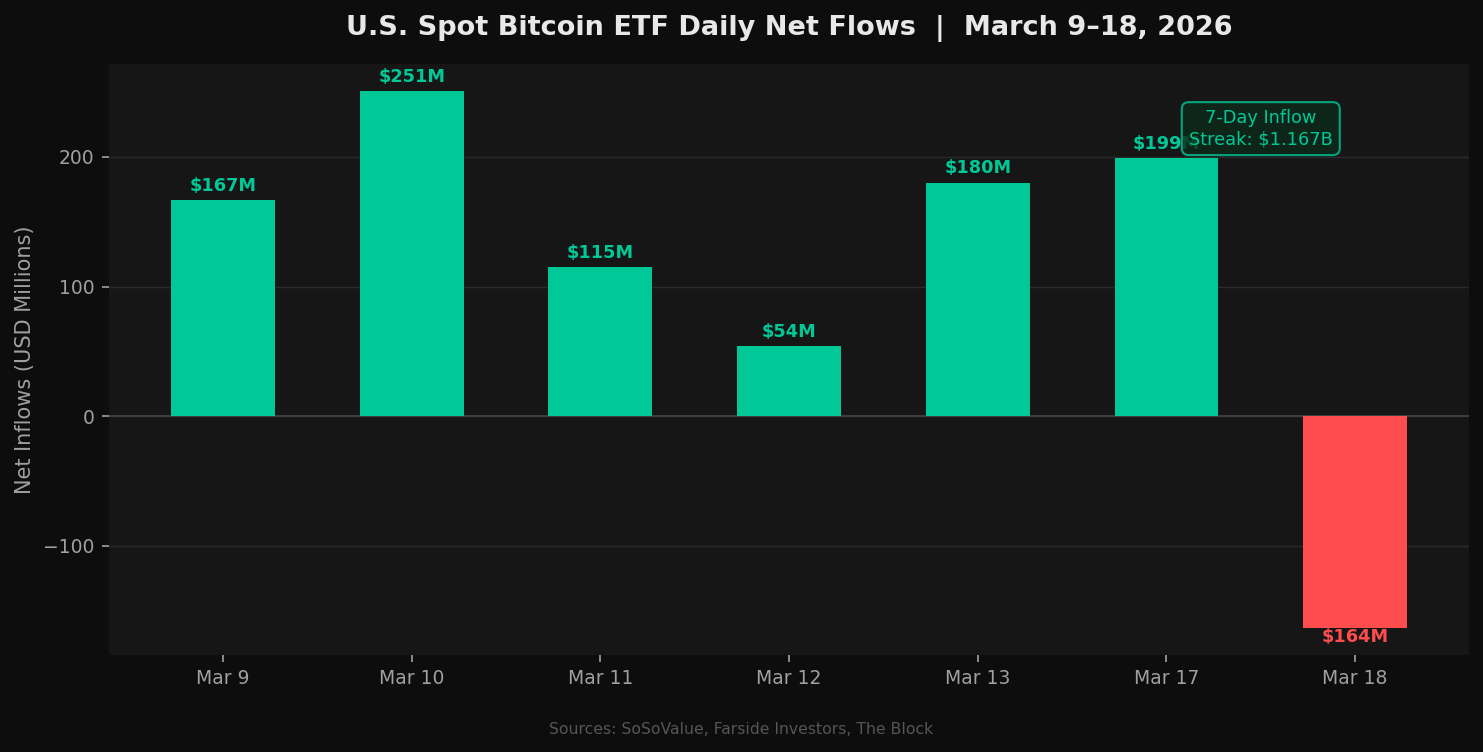

The Federal Reserve held rates steady at 3.50%-3.75% on March 18, maintaining its December projection of one rate cut in 2026 while revising its inflation forecast upward to 2.7% core PCE. Bitcoin fell sharply after Powell’s press conference, and U.S. spot Bitcoin ETFs recorded $163.5 million in outflows on March 18, reversing a seven-day inflow streak that had pulled in $1.167 billion.

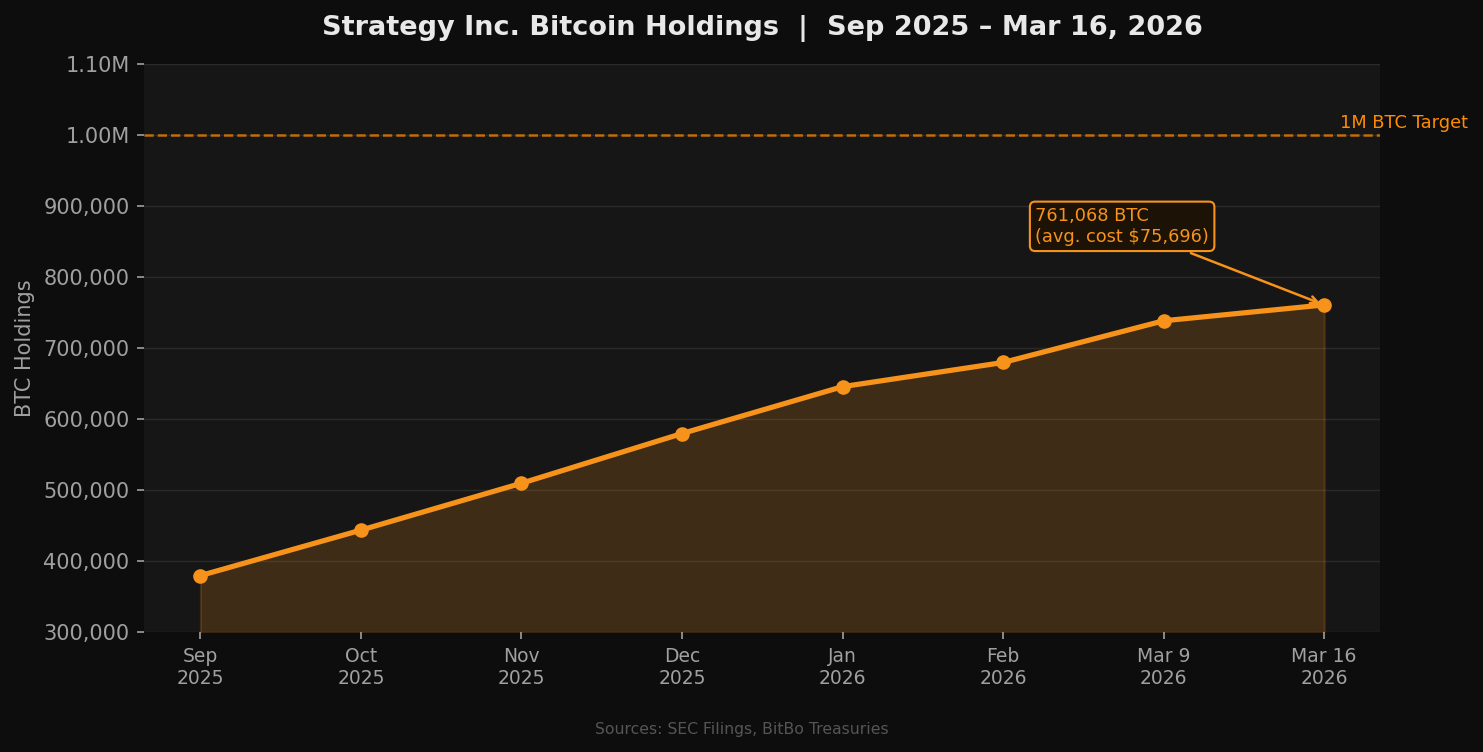

Strategy (formerly MicroStrategy) executed its largest single-week Bitcoin acquisition of 2026 during March 9-15, purchasing 22,337 BTC for approximately $1.57 billion at $70,194 per coin, bringing total holdings to 761,068 BTC with an average cost of $75,696 per coin, with a total cost of approximately $57.61 billion.

Bitcoin traded near $68,014 on March 23, down from a 40-day high of approximately $74,300 hit in mid-March, as Powell’s hawkish press conference and upward inflation revisions pushed prices back toward the $67,500-$70,000 support band.

The CLARITY Act advanced meaningfully: Senators Tillis and Alsobrooks reached a tentative compromise on stablecoin yield on March 20, with Polymarket pricing passage odds at approximately 65-72%. Four sequential legislative steps remain before the bill reaches the President’s desk.

XRP surged to $1.60 on March 17 following the SEC/CFTC commodity classification, before settling near $1.50 after the Fed’s upward inflation revisions. The March 27 deadline for spot XRP ETF applications represents the next major binary catalyst.

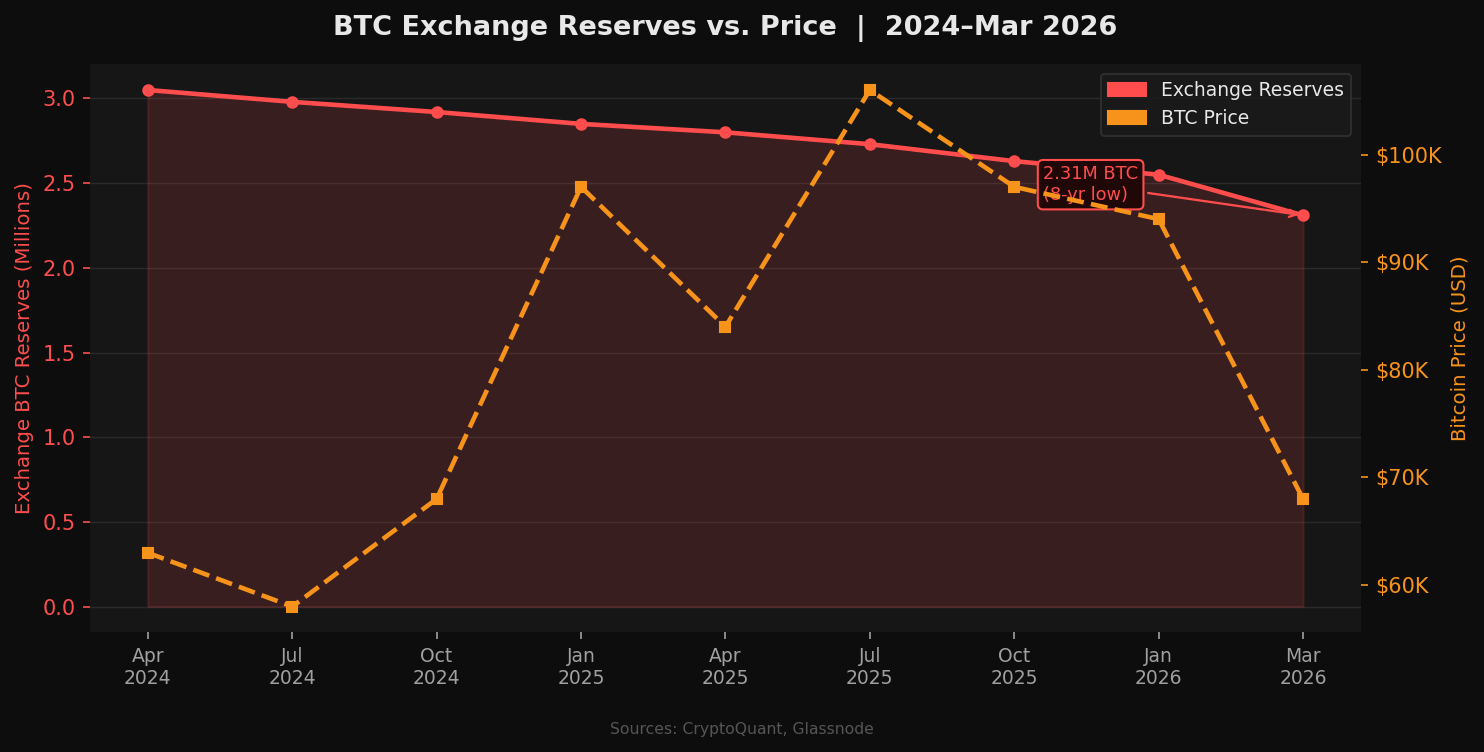

Bitcoin exchange reserves fell to approximately 2.31 million BTC, the lowest level since April 2018, as long-term holders continue moving coins into self-custody at a historically elevated pace.

1. Weekly Opening Insight

Two forces collided in crypto markets this week, and neither yielded without a fight. On Monday, the SEC and CFTC jointly published the most consequential piece of regulatory clarity the U.S. has ever produced for digital assets, officially classifying 16 major cryptocurrencies as digital commodities under CFTC jurisdiction. By Wednesday, the Federal Reserve had reminded markets why clarity alone cannot override liquidity, as Powell’s press conference and upward inflation revisions pushed Bitcoin from above $74,000 back toward $68,000 in a matter of hours.

The week illustrated something important about crypto’s 2026 structural reality. The market is no longer a binary risk-on/risk-off vehicle that moves purely with equities. It has regulatory tailwinds, institutional demand anchors through ETFs, and corporate treasury buyers operating on weekly accumulation schedules. But it still reprices sharply when inflation expectations rise, and the Fed’s revised core PCE forecast of 2.7% is the clearest signal, yet the easing cycle is on hold.

What makes this moment analytically interesting is the layering. Regulatory clarity, improving legislative momentum, and an on-chain supply picture that looks historically tight…all of these are building a floor. But the ceiling is capped by a Fed that has maintained just one projected cut in 2026 against a backdrop of rising oil and inflation, and a political backdrop in Washington that could still delay the CLARITY Act past the midterm window. Here’s what crypto investors should understand about the week ahead.

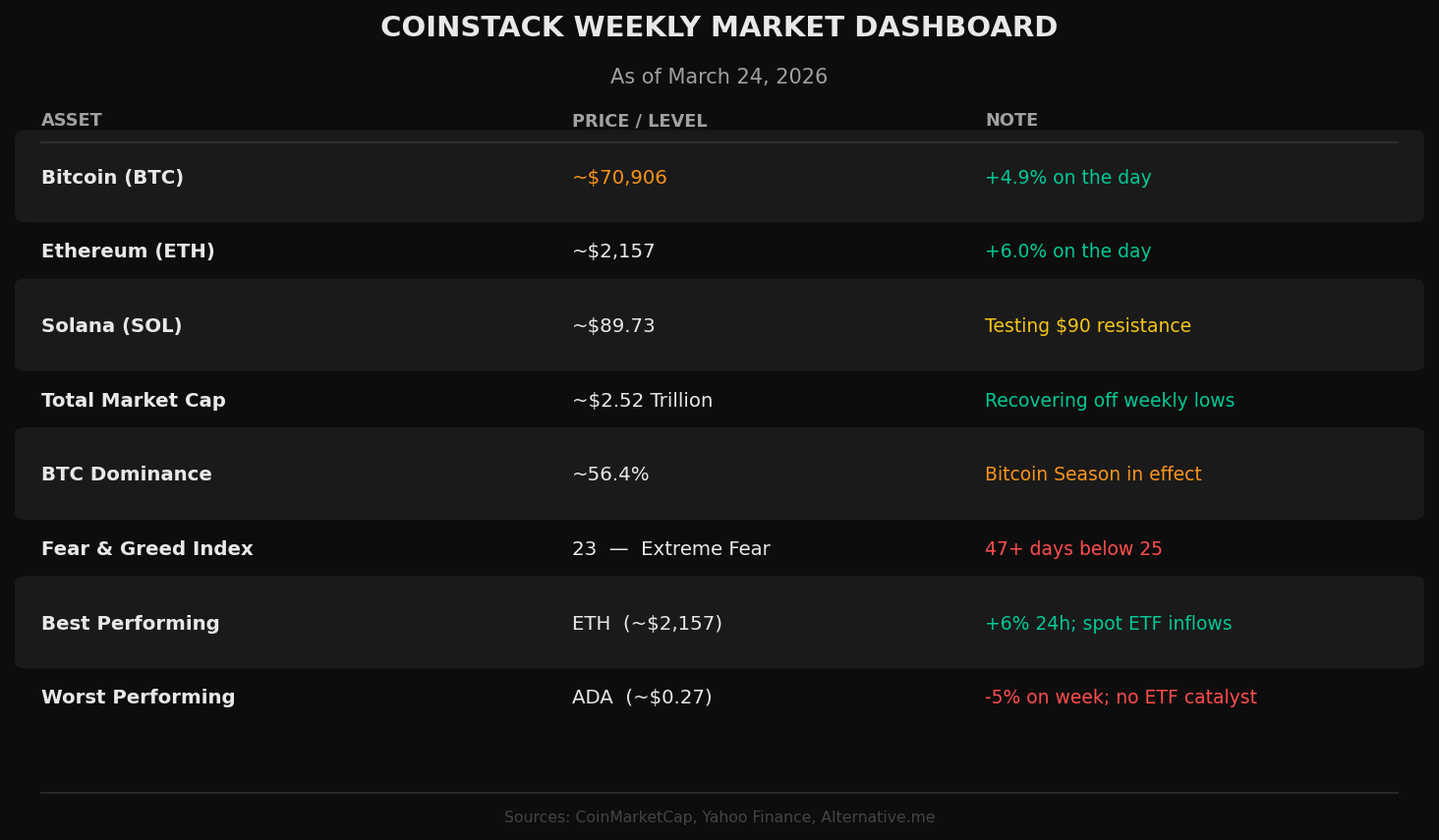

2. Weekly Market Dashboard

Best Performing Large-Cap: XRP ($1.44, week of high: $1.60).

XRP was the standout performer of the regulatory week, surging to $1.60 on March 17 following the SEC/CFTC taxonomy release, rising 9.8% on the weekly chart at its peak, accompanied by a 112% surge in 24-hour trading volume to $3.66 billion, the kind of volume expansion that signals genuine accumulation rather than price drift. The catalyst was the explicit classification of XRP as a digital commodity under CFTC jurisdiction, removing the legal overhang that had weighed on the asset since 2020. The gains partially reversed after the Fed’s inflation revision on March 18, with XRP settling near $1.44 as of March 24, reflecting a -4.8% pullback over the trailing 7 days, a pattern where the regulatory repricing held structurally but the macro-driven selloff trimmed the weekly peak.

Watch March 27: That is the SEC’s deadline on the latest batch of spot XRP ETF applications. With commodity status now formally in place, the statutory basis for denial is materially weaker than at any prior point in the case’s history.

Worst Performing Large-Cap: Cardano (ADA, $0.26, -8% on the week)

ADA traded near $0.26 as of March 23, down approximately 8% on the week, underperforming broader category momentum significantly, and sitting more than 90% below its all-time high of $3.10. Despite being formally reclassified as a digital commodity in the March 17 ruling, which should have been a tailwind, ADA failed to sustain any meaningful bounce. Volatility actually compressed rather than expanded after the ruling, with volume down 15% from the prior week, suggesting the market is treating the classification as necessary but insufficient on its own. The structural tension is clear: ADA’s price sits below its 50-day and 200-day SMAs, both declining, while the $0.2676 level has become the most-tested support floor. There are legitimate catalysts on the horizon: the Midnight privacy sidechain mainnet is due in the final week of March, with the van Rossem hard fork following in April, but without a credible spot ETF filing gaining traction, ADA’s regulatory tailwind is unlikely to translate into sustained price recovery in the near term.

What drove markets this week: The dominant narrative was regulatory optimism colliding with macro reality. Bitcoin briefly cleared $74,000 following the SEC/CFTC taxonomy release, before Powell’s March 18 press conference, and the upward revision to the 2026 inflation forecast reversed sentiment and sent BTC back toward $68,000. The net result was a week that felt bullish in tone but finished lower in price, a pattern that reflects a market still working through macro headwinds even as its structural foundations improve. ETF flows provided clear evidence of the sentiment reversal: a seven-day inflow streak worth $1.167 billion ended abruptly with a $163.5 million outflow on March 18, the same day Powell spoke.

3. The Big Story of the Week

SEC Releases Landmark Crypto Framework in Coordination With CFTC, Covering 16 Major Assets

What happened:

On March 17, 2026, the Securities and Exchange Commission published a 68-page interpretive guidance in coordination with the Commodity Futures Trading Commission, establishing the first official U.S. taxonomy for digital assets. The framework sorts crypto assets into five categories: digital commodities, digital collectibles, digital tools, payment stablecoins, and digital securities.

Sixteen major assets were formally classified as digital commodities subject to CFTC oversight: Bitcoin (BTC), Ethereum (ETH), XRP, Solana (SOL), Cardano (ADA), Chainlink (LINK), Dogecoin (DOGE), Avalanche (AVAX), Polkadot (DOT), Hedera (HBAR), Litecoin (LTC), Bitcoin Cash (BCH), Shiba Inu (SHIB), Stellar (XLM), Tezos (XTZ), and Aptos (APT). Algorand (ALGO) and LBRY Credits (LBC) were cited as additional examples in the document footnotes. Sitting SEC Chairman Paul Atkins said at the DC Blockchain Summit: “We’re not the ‘securities and everything commission’ anymore.”

Why it matters:

The downstream implications are immediate and structural. Financial institutions that previously treated assets like XRP, Solana, and Cardano as potential unregistered securities, a compliance posture that limited custody services, exchange listings, and institutional product development, now have a clear federal framework under which to operate. Compliance departments can shift from securities registration requirements to the comparatively standard commodity reporting framework, removing one of the largest operational barriers to institutional participation in altcoin markets. This classification also clears the regulatory path for additional spot ETF products.

Investor takeaway:

The key distinction to understand is that this ruling is an interpretive release, not legislation. The CLARITY Act, currently advancing in the Senate, is required to codify this taxonomy permanently under federal law. If the bill stalls, the commodity classification remains legally vulnerable to future policy reversal. Watch whether the Senate Banking Committee proceeds to markup by late April, as Senator Moreno has warned that failure to advance by May could delay meaningful digital asset legislation for years. The March 27 XRP ETF deadline is the immediate binary event.

4. Key Market Developments

FED Holds Rates, Revises Inflation Higher: Bitcoin’s 7-Day ETF Inflow Streak Ends With $163.5 Million In Outflows

What happened: The Federal Reserve held rates steady at 3.50%-3.75% on March 18, as expected. The updated dot plot maintained the December projection of one rate cut in 2026, unchanged at the median, but the balance of individual projections shifted marginally more hawkish, with seven FOMC members now projecting no cuts versus six in December. More materially, the committee revised its 2026 core PCE inflation forecast upward from 2.5% to 2.7%, and Powell said during the press conference that the Fed has “not made as much progress on inflation as it had hoped,” pointing to elevated oil prices from the Middle East conflict as a key uncertainty. Bitcoin dropped sharply in the hours following Powell’s remarks. U.S. spot Bitcoin ETFs recorded $163.5 million in net outflows on March 18, ending seven consecutive days of inflows that had totaled $1.167 billion from March 9 through March 17. Fidelity’s FBTC led outflows at $103.8 million, followed by BlackRock’s IBIT and Grayscale’s GBTC.

Bull case: A single outflow session does not erase the structural trend. Bitcoin ETFs still absorbed a net $1.167 billion over the preceding seven-session streak. Total cumulative net inflows across all U.S. spot Bitcoin ETFs stood at $56.41 billion as of March 18, with total net assets near $96.74 billion. If April CPI data shows inflation softening, the market will rapidly reprice rate cut expectations, and ETF flows are likely to accelerate.

Bear case: The median dot plot projection of one cut was unchanged, but the inflation revision to 2.7% core PCE signals the Fed’s tolerance for price pressure has not expanded. Powell’s term expires in May, and his likely successor, Kevin Warsh, is considered more hawkish. If the incoming Fed leadership maintains a restrictive posture into Q3 2026, risk assets, including Bitcoin, will face a persistent headwind, and ETF inflows may remain inconsistent.

Strategy Executes Largest Single-Week Bitcoin Purchase of 2026

What happened: During the week of March 9-15, Strategy (formerly MicroStrategy) purchased 22,337 BTC for approximately $1.57 billion at an average price of $70,194 per coin, its fifth-largest single-week acquisition ever and largest of 2026. The purchase was funded primarily through $1.18 billion in STRC perpetual preferred stock sales, alongside $396 million raised through 2.8 million Class A common shares.

Strategy’s total Bitcoin treasury stands at 761,068.

BTC, as of March 15, acquired at an average cost of $75,696 per BTC for a total of approximately $57.61 billion. The company is targeting 1 million BTC by year-end, which would require purchasing approximately 5,700 BTC per week for the remainder of 2026.

Bull case: Strategy’s accumulation pace is functioning as a structural supply drain. At current purchase rates, the company absorbs weeks of newly mined Bitcoin in single sessions. Its preferred stock vehicles, STRC, in particular, carry an 11.5% annual yield, providing a scalable capital-raising mechanism that does not require Bitcoin price appreciation to execute. Each purchase compresses the float of tradable Bitcoin on exchanges.

Bear case: Strategy’s aggregate average cost of $75,696 per coin means current Bitcoin prices near $68,000 represent a meaningful unrealized loss on the treasury. Continued equity dilution also weighs on common shareholders as the company issues millions of new MSTR shares each week. If Bitcoin remains below the average cost basis for an extended period, the financial dynamics of the preferred stock Strategy will face closer scrutiny from equity holders.

Clarity Act Stablecoin Impasse Breaks: 4 Steps Still Remain

What happened: Senators Thom Tillis and Angela Alsobrooks reached a tentative compromise on stablecoin yield on March 20. The issue that had stalled the CLARITY Act’s advance in the Senate since January’s canceled markup. The deal prohibits passive stablecoin yield (paid simply for holding a token balance) but permits activity-based rewards tied to payments, transfers, and platform usage. Senator Tillis said the talks are “in a good place,” while Senator Lummis said at the DC Blockchain Summit the bill is “so close” to passage. White House Crypto Council Executive Director Patrick Witt called the development a “major milestone.” A separate complication emerged as Senate Republicans discussed attaching community bank deregulation provisions to the bill. Senator Moreno warned that failure to advance by May could effectively kill digital asset legislation before the midterm election cycle takes over the congressional calendar. Polymarket currently prices 2026 passage odds at approximately 65-72%.

Bull case: The stablecoin yield compromise removes what had been the most intractable technical disagreement. The CLARITY Act passed the House 294-134, signaling a strong bipartisan appetite. If the Senate Banking Committee markup proceeds by late April as expected, the legislative window before midterms will remain viable.

Bear case: 4 sequential steps remain…Senate Banking Committee markup, a Senate floor vote requiring 60 votes, reconciliation with the Agriculture Committee version, and a presidential signature. DeFi liability language and ethics provisions related to elected officials’ personal crypto holdings remain unresolved. The Senate calendar is compressed, and midterm dynamics could push crypto legislation down the priority list.

5. On-Chain Data Insight

Bitcoin Exchange Reserves Hit Lowest Level Since April 2018 As Whale Accumulation Accelerates

The Data:

Bitcoin exchange reserves fell to approximately 2.31 million BTC as of mid-March 2026, according to on-chain data from CryptoQuant and Glassnode, the lowest level since April 2018. Whale wallets accumulated approximately 270,000 BTC during the extended extreme fear period, representing the largest net purchase by this cohort in over 13 years. The Fear and Greed Index sat at 23 (Extreme Fear) as of March 19, with the market having spent more than 46 consecutive days in Extreme Fear as of Early/Mid-March 2026.

What the data shows:

Coins leaving exchanges move into self-custody, cold storage, or long-term holding wallets. They are removed from the immediately tradable float and cannot be instantly sold on order books. With only 2.31 million BTC remaining on exchanges, the effective liquidity available for sellers has compressed to levels not seen in eight years. The current setup means that even modest increases in demand, whether from ETF inflows, corporate treasury purchases, or retail re-entry, are met with substantially less supply than at any recent point in the cycle.

What it might signal:

The combination of declining exchange reserves, the lowest Fear and Greed readings in the index’s history earlier this year, and sustained whale accumulation at elevated prices is a confluence rarely observed simultaneously. On-chain data from Glassnode shows that purchasing Bitcoin when the Fear and Greed Index drops below 25 has yielded a median 90-day return of approximately 38% historically. This is not a guarantee of future performance, and the 2022 bear market showed that extreme fear can persist for extended periods while prices continue declining. But the structural fingerprint, smart money accumulating, retail exiting, exchange reserves thinning, closely mirrors the setup observed in Q1 2023 and Q4 2024, both of which preceded significant price appreciation within 90 days.

6. Narrative Watch

Regulatory Clarity As A Demand Multiplier: The Market Is Pricing In What Comes Next

The Narrative:

For years, the regulatory cloud over assets like XRP, Solana, and Cardano was a structural barrier to institutional capital. Compliance departments, ETF applicants, and custody providers all had to treat these assets as potential unregistered securities. The SEC/CFTC joint taxonomy on March 17 did not just remove a legal question; it unlocked an entire category of institutional infrastructure that can now be built without regulatory risk. The market is beginning to price this in.

Why it’s gaining attention:

The immediate evidence is XRP’s price response and the accelerating ETF approval pipeline. Spot XRP ETFs are already at $1.44 billion in cumulative inflows, and now face a final approval decision by March 27 with no plausible statutory grounds for SEC denial. Beyond XRP, the commodity classification opens doors for tokenized versions of all named assets, new leveraged and options products, and integration into traditional brokerage platforms, where compliance teams previously had to maintain securities-era restrictions.

Why it could grow:

The CLARITY Act, if passed, would codify this taxonomy into permanent law and provide the statutory backstop that Chairman Atkins himself has called necessary to make these interpretations durable. If the bill advances to Senate markup in April as currently expected, the narrative will shift from “regulatory clarity in principle” to “regulatory clarity in law,” a distinction that carries more institutional weight.

Why it could fade:

The interpretive release carries explicit legal caveats: it is not legislation, and a future administration or agency leadership change could reverse it. If the CLARITY Act stalls past May, the window for meaningful 2026 legislation closes, and markets will need to reassess the durability of the current regulatory posture.

7. Investment Theme of the Week

The Second-Layer Commodity Play: Altcoins Newly Re-Classified As Digital Commodities

The Opportunity:

When 16 crypto assets are officially reclassified from securities risk to commodity status, the repricing is not instantaneous. Institutional capital moves through compliance reviews, custody approvals, and product launches, all processes that take weeks to months, not hours. This creates a window where assets like Solana, Cardano, Avalanche, Chainlink, and Algorand are legally reclassified, but institutional infrastructure has not yet caught up. Historically, this type of regulatory de-risking event, where the legal barrier drops before the institutional flow arrives, has represented a durable entry point for patient capital.

Thesis:

The commodity classification removes the single largest structural barrier to institutional participation in these assets: securities law compliance risk. Custody providers, ETF applicants, and regulated funds can now approach all 16 named assets using the commodity compliance framework, which is materially simpler than securities registration. The assets most likely to see the fastest institutional re-engagement are those with existing ETF filings (Solana) or large pre-existing institutional interest (Chainlink, Avalanche).

Catalysts:

The March 27 XRP ETF deadline is the first binary event. Additional spot ETF approvals for Solana, Cardano, or Avalanche could each function as regulatory milestones that unlock a new pool of demand. CLARITY Act Senate markup proceedings in late April or May would be the most powerful single catalyst across the entire commodity-classified asset basket. Any softening in Fed language at the May FOMC meeting would add a macro tailwind to what is currently a fundamentally-driven thesis.

Risks:

The interpretive release is not law. A reversal of the current SEC/CFTC posture by future agency leadership would reintroduce the compliance barriers that currently cap these assets. Not all 16 commodity-classified assets have equal liquidity, developer activity, or institutional-grade custody infrastructure. And if macro conditions deteriorate significantly, sustained elevated inflation, a second round of tariff escalation, or a geopolitical liquidity shock, these assets will sell off alongside everything else, regardless of their regulatory status.

8. Smart Crypto Insight

Understanding The Dot Plot: Why A Single Fed Chart Moved Crypto More Than The Rate Decision Itself

Every FOMC meeting includes a press conference and a rate decision. But four times a year, the Fed also releases the Summary of Economic Projections, which includes the “dot plot,” a chart showing where each of the 19 FOMC members individually expects interest rates to go over the next several years. This week, what the dot plot revealed was that inflation expectations mattered more than the rate decision.

Here is why. The rate decision was held steady at 3.50%-3.75%, which virtually everyone expected. The median dot projection for 2026 also held steady at one cut, the same as December. But a closer look showed seven members now projecting no cuts at all, one more than in December. More importantly, the 2026 core PCE inflation forecast was revised upward from 2.5% to 2.7%. That inflation revision, combined with Powell’s comments about limited progress on price stability and uncertainty around the Middle East conflict, was the actual catalyst for the crypto sell-off that followed.

The practical implication for crypto investors is this: when the inflation revision moves higher in a dot plot, ETF inflows tend to slow or reverse within 48 hours, because institutional portfolio allocators are rebalancing their risk exposure. The $163.5 million outflow on March 18 was a direct and measurable expression of that repricing. For investors managing around the Fed calendar, the inflation projections in the dot plot, not just the rate decision itself…are the variables to model closely.

9. Quick Hits from the Week

The XRPL integrated native AI agent payment capabilities on March 21, allowing autonomous AI systems to transact directly using XRP, expanding the ledger’s utility into the emerging agent commerce market.

Bitcoin mining difficulty dropped 7.7% to 133.79 trillion in the latest adjustment, the sharpest single-period decline since February 2026, as elevated energy costs and lower BTC prices push marginal miners offline.

Approximately $2.1 billion in Bitcoin and Ethereum options expired on March 20, coinciding with Wall Street’s $5.7 trillion quarterly “Triple Witching” expiry event, with ETH’s max pain point sitting near $2,150, close to the spot price.

Grayscale formally proposed bringing Hyperliquid’s HYPE token to traditional brokerage accounts through a planned ETF filing, citing the network’s $50 billion weekly derivatives trading volume and $1.6 million in 24-hour fee revenue as justification.

Phantom Wallet received a no-action letter from the CFTC on March 18, allowing it to serve as a non-custodial interface connecting users to registered derivatives platforms without requiring broker registration, a meaningful step toward regulated DeFi access for U.S. users.

The Federal Reserve payment system formally granted Kraken Financial (the banking arm of crypto exchange Kraken) access in early March via a limited-purpose account, marking the first formal integration of a crypto firm into the Fed’s core payment infrastructure (e.g., direct Fedwire connectivity without intermediary banks).

10. Closing Macro Thought

Eighteen months from now, March 2026 may be remembered as the turning point when everything changed structurally. The SEC and CFTC jointly reclassified 16 assets as digital commodities. The CLARITY Act’s most contentious provision was effectively resolved. Bitcoin exchange reserves fell to an eight-year low while institutional buyers absorbed supply at a weekly cadence. The Fear and Greed Index spent more consecutive days in Extreme Fear than at any prior point in crypto history, while smart money was net buying.

And yet the price action looks unremarkable. Bitcoin finished the week near its entry point. Sentiment remains deeply negative. The Fed reminded everyone that one projected rate cut means exactly that, one, and an inflation forecast that moved from 2.5% to 2.7% core PCE is not a trivial revision when oil is above $95, and Middle East tensions remain unresolved. None of this resolves quickly.

What makes the current moment structurally different from prior cycles is that the accumulation is happening in plain sight, by identifiable institutional actors, with published regulatory backing, at the same time that the supply available to sell is at its lowest in eight years. Prior capitulation episodes were characterized by retail holders selling to unknown buyers. This one is characterized by whale wallets and corporate treasuries buying in size while Fear and Greed scores single digits.

The macro ceiling is real. But the structural floor is built in a way that has no clear historical precedent. Watch the March 27 XRP ETF decision, watch whether the Senate Banking Committee schedules a markup date in April, and watch what happens to ETF flows in the first week following the next CPI print. The market is assembling the conditions for something. The question is only how long the macro ceiling holds it down.

Coinstack is published every Tuesday. Nothing in this newsletter constitutes financial or investment advice. All information is sourced from publicly available data and should be independently verified.

© 2026 Coinstack. All rights reserved.